✈️ The Concorde: Euro leaves the dollar in the dust

Your September 28 transatlantic news roundup.

I spent the weekend in beautiful Bonn, Germany, home to a surprisingly large number of international organizations for a city of only 300,000 people. Why? It’s a holdover of when the city on the Rhine was the capital of West Germany. That was a tactical choice over the much larger Frankfurt to avoid creating the impression of a permanent West German capital, which could have undermined support for German reunification. Talk about smart thinking ahead…

In today’s Concorde…

— A group of left-leaning political leaders from both sides of the Atlantic met in London to discuss what a new progressive political agenda could look like.

— The euro looks poised to continue strengthening against the dollar, with major banks projecting it to hit $1.25 within a year.

— After years of talk and waning American financial support, Europe appears ready to finally seize Russian assets to finance the Ukrainian war effort.

Driving the week

LEFT RESURGENCE? — An “industrialised infrastructure of grievance.” That’s what British PM Keir Starmer called the power of right-wing populist rhetoric at a conference in London this week. The Global Progress Action Summit brought together left-leaning leaders from across the world to discuss strengthening their message against populism, what a new governing agenda for the left could look like, and how nationalism could play a role in left-wing politics. Aside from Starmer, speakers and attendees included Canadian PM Mark Carney, Australian PM Anthony Albanese, Danish PM Mette Frederiksen, and Pete Buttigieg and JB Pritzker from the United States.

The think tank that organized the summit hoped that it would be “the start of a progressive reinvention — that drives a fairer, more prosperous and more sustainable world.” One perspective pushed at the summit was that the center-left needs to take back the “flag” and a national sense of place from more populist elements. That’s becoming increasingly important in the United Kingdom, where flag flying and national anti-immigration protests have spread rapidly throughout the country, and with Nigel Farage’s Reform UK party rocketing ahead in the polls.

EURO RISING — The euro has already strengthened significantly against the dollar this year, and if banking analysts are right it’s poised to grow even stronger in the year to come. Major banks like Goldman Sachs, JPMorgan and UBS believe that the euro could rise up to $1.25 this year. To put that in perspective, the euro was worth about $1 around the time of Trump’s inauguration in January of this year. On Friday, it was worth about $1.17, an increase of 17 percent. If the euro reaches $1.25, it would be hitting levels not seen since 2014. Fundamentally, the increase in the euro’s price is a reflection of more concern about the US economy under Trump’s tariff regime, and a reflection that Europe might be a better place to hold currency.

While the European Central Bank is excited about the prospect of such a strong euro, saying that it “would bring tangible benefits” such as lower borrowing costs, reduced exposure to currency shifts, and protection from sanctions. That said, the euro’s strengthening (and the dollar’s weakening) is actually part of Trump’s plan to help American reindustrialization efforts. A stronger euro means American goods are cheaper for European consumers to buy. The flip side is that European exports to the US will become much more expensive. That’s a major concern for European industry — such as the much-discussed and oft-maligned German automakers — who would have more trouble selling their cars in the US.

ASSET SEIZURE GO TIME — After years of cold feet, Europe finally seems poised to use the ~$330 billion in frozen Russian assets sitting in European banks to fund Ukraine’s war effort. Although it’s not a done deal yet, the op-ed published by German PM Friedrich Merz in the Financial Times this week showed that Germany — long resistant to touching Russian assets — was finally ready to support a plan. Why the shift? The Americans will no longer directly fund Ukraine with military aid, and Ukraine has a huge budget deficit to fill. As Timothy Ash writes in his excellent primer on the topic, “Europe is on the hook for the full $100 billion plus per annum in costs of keeping Ukraine in the war… and European taxpayers cannot be expected to pay a $100 billion a year bill…”

But there are more hurdles to jump than just Germany to bring the plan to fruition. First, Merz and other leaders aren’t actually proposing to seize the assets directly. That would be a violation of international law and sovereign immunity, and could open Europe and Belgium — the home of Euroclear, which holds the majority of Russian assets — at legal risk. Instead, the European plan is to use a series of bonds backed by the Russian assets to fund Ukraine with interest-free loans. Hypothetically, that would keep the Russian assets intact, reducing the risk of legal challenges, while also providing enough backing for massive bonds to fund Ukraine’s war effort.

Second, there’s still significant opposition from within Europe to the plan. Belgian PM Bart de Wever said this week that “Taking Putin’s money and leaving the risks with us. That’s not going to happen, let me be very clear about that.” He’s worried that Belgium could face arbitration claims. Others believe that seizing the assets could lead to a loss of trust in Europe as a safe haven for foreign investment, hurting the euro and bloc’s economic prospects. However, Europe is trapped between a rock and a hard place. Without American support, they must come up with more funds to support the Ukrainian war effort. Ultimately, the choice is between European or Russian taxpayer money. While it might take more finagling, in the end Europe will figure out how to leverage the Russian money over its own.

In review

European homicide rates are tiny compared to those in America

Over the past year, Brussels has been caught up in a crime spree. Or at least, that’s what you’d think if you’re reading the local news.

Brussels is a “dangerous city,” and the Belgium federal government is considering deploying the military to patrol the streets. “After a summer of brutal violence and two deaths in Brussels,” wrote the expat-oriented English language paper The Brussels Times, the interior minister “wants more police, more cameras and soldiers…”

But a closer look at the numbers — especially in transatlantic comparison — tells a very different story. Brussels, and European cities writ large, are miraculously safe compared to their American counterparts.

How to make transatlanticism cool again

In the 21st century attention matters more than ever before. Attention, as Kyla Scanlon and Tim Wu argue, is a basic resource of this century, not so different from land, labor, or capital in centuries past. It’s attention, Scanlon says, that “determines what gets funded, elected, or built… Shape the feed, shape the future.”

That’s a big problem for transatlanticism.

The great attention brokers and generators of the 21st century — Trump, X, MAGA, Facebook, and influencers of the political left, to name a few — don’t care one whit for transatlanticism. They find that transatlanticism isn’t flashy enough, interesting enough, or controversial enough to generate the attentional capital that would justify their time.

Even those who want to celebrate transatlanticism — most prominently in recent years Joe Biden — have or are now finding it difficult to craft narratives that direct attention to the concept.

In the past two weeks I also published a piece that digs into the EU-US trade deal with the Parliament Magazine and a piece with Transformer on staffing challenges at the EU AI Office. Read the pieces below.

Why the EU’s $1.35 trillion deal with Trump is an impossible promise

Brussels sold its US trade deal as transatlantic unity and a path away from Russian energy. But the fine print reveals a different story: energy the US can’t supply and investments Brussels can’t deliver.

Tweet to read

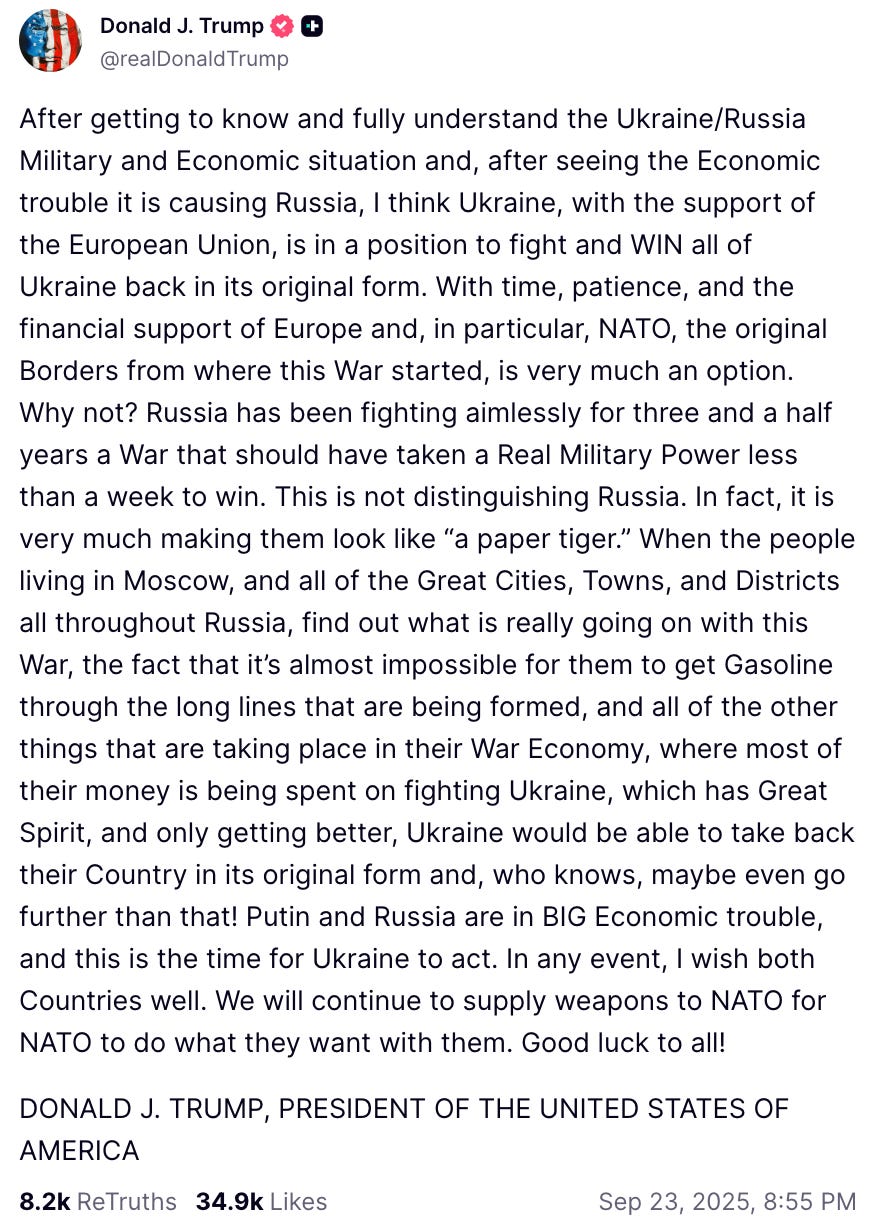

Trump’s declaration from the United Nations meeting earlier this week that Ukraine could win back its original borders is causing heads to spin in Europe. One theory of the case? That Trump is trying to wash his hands of a war he knows he can’t end.

Number of the week: $1.57

That’s the highest value of the euro against the dollar in the currency’s history. It hit that value in 2008, after the US financial crisis and the start of the Great Recession led investors to move their money into euro-denominated assets. Higher ECB interest rates and a pre-Eurozone crisis belief in European stability also made the euro a more attractive currency at the time.

What I’m reading on transatlanticism

GREENLANDIC HISTORY — For Foreign Exchanges, Gretchen Heefner wrote an excellent primer on the long history of American involvement in Greenland that stretches long before Trump had his eyes on the icy island. She writes that America’s 70-year history in Greenland has “been mostly bad for Greenland and a mind-bogglingly expensive quixotic venture for” the US.

EUROPE’S TRUMP WHISPERER — Italian PM Giorgia Meloni gave a novel speech at the United Nations conference in New York this week that reflected her unique role within the transatlantic relationship. She’s a far-right leader who is willing to work within the European Union, but also able to speak the language of Trump. The way she framed her speech reflected those dual interests and role — in a brisk fifteen minutes she was able to condemn Russia’s war in Ukraine while attacking European climate politics and calling for stronger resistance to migration.

The return on investment in the US is far greater than in Europe. US corporations and investors are taxed less than in Europe, and there are far fewer regulations. As a result, investment in US tech is far greater. We also attract the best tech workers from other countries.

Peder, excellent explanation of the situation with the Euro. I think it will be very interesting to see how this fits within the EU's broader approach to competitiveness, especially the Savings & Investments Union and the Banking Union. How do you see this evolving?